GIFT City Fixed Deposit Product

Get in touch to start

Frequently Asked Questions (FAQs)

1. Who can invest in this FD?

This FD is designed for Non‑Resident Indians (NRIs) and Overseas Citizens of India (OCIs) who hold valid KYC documents and are eligible to invest in GIFT City products under RBI/IFSCA rules. It is particularly targeted at NRIs earning or holding savings in USD (for example in the US, Canada, UK, EU, Middle East etc.).

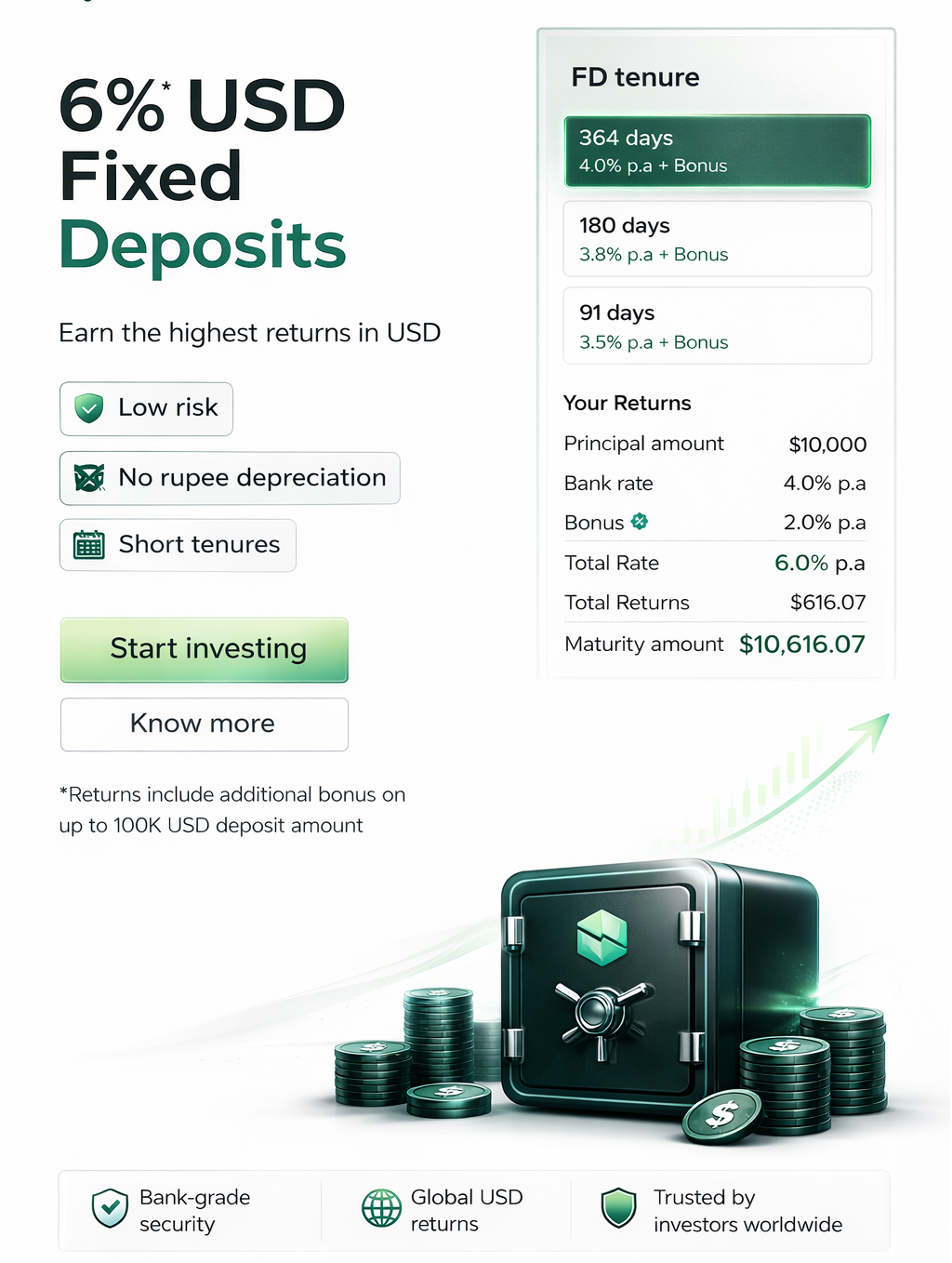

2. Is 6% guaranteed? Can rates change?

No platform can permanently guarantee a specific rate; FD rates are set by the partner bank and can change over time. Once your FD is booked at a confirmed rate for a given tenor, that contracted rate is normally fixed for that deposit unless you break it early, in which case RBL Bank’s premature‑withdrawal penalties apply.

3. Who is the actual bank behind this FD?

The underlying FD is with RBL Bank’s GIFT City IFSC branch, which is regulated by IFSCA in GIFT City and by RBI in India. Belong itself is not a bank; it is a regulated fintech platform that facilitates the account opening and FD booking journey with its partner banks.

4. How is this different from a normal NRE or FCNR FD?

In a normal NRE FD, you earn interest in INR and are exposed to INR depreciation versus USD, so a 6.5% INR NRE FD may be closer to ~3% in USD terms after currency effects. In this GIFT City USD FD, your principal and returns are denominated in US dollars, which can better match your USD liabilities and avoids INR currency risk on that portion of your portfolio.

5. Is interest tax‑free?

Under India’s current GIFT City and IFSC framework, interest on qualifying foreign‑currency FDs for eligible NRIs/OCIs in GIFT City is not taxed in India. You still remain liable for tax in your country of residence, so this FD should be reported as foreign income where required (for example, in the US), and local tax treatment will depend on your personal situation.

6. What about TDS or withholding tax in India?

For eligible NRI/OCI investors in GIFT City foreign currency FDs, there is usually no Indian TDS or withholding on the FD interest, in line with the current IFSC rules and tax incentives. However, tax rules can change and you should confirm the latest position with Belong, RBL Bank or your tax adviser before investing.

7. Is the FD fully repatriable?

Deposits are held in USD with RBL Bank’s GIFT City branch and are intended to be fully repatriable, meaning both principal and interest can be remitted back overseas, subject to applicable KYC and banking procedures. Exact remittance mechanics, timelines and any fees are governed by RBL Bank’s GIFT City terms and Indian FX regulations.

8. What documents are typically required?

While exact requirements can vary, GIFT City NRI FDs generally require:

Passport,

Valid visa / residence permit,

PAN (or alternative as allowed),

Overseas address proof,

FATCA/CRS declarations. Belong and RBL Bank will specify the exact KYC list during onboarding in line with IFSCA/RBI rules.

9. What happens if I need to break the FD early?

Premature closure is usually allowed but subject to a penalty on the contracted rate, often around 100 basis points (1%) or as per the bank’s premature‑withdrawal grid for GIFT City deposits. The exact penalty, minimum holding period and whether any bonus component is forfeited are governed by RBL Bank’s GIFT City FD terms at the time of booking.

10. What is IFSC / GIFT City?

GIFT City (Gujarat International Finance Tec-City) is India’s first International Financial Services Centre (IFSC), designed as an offshore-style financial hub within India where transactions are done in foreign currency under a separate regulator, IFSCA.

11. What is video KYC / V‑CIP in GIFT City?

Video KYC (V‑CIP) is a regulated, video-based process where the bank verifies your identity and documents over a secure video call instead of a physical visit, with liveness checks and geo-tagging.

Important Disclaimer: NuQuant B.V. (“NuQuant”) does not have any commercial, partnership, or referral agreements with Belong or its affiliates. The information shared about Belong’s USD Fixed Deposits is provided solely for reference, educational purposes, and knowledge sharing to benefit users interested in GIFT City investment options. NuQuant makes no representations, warranties, or endorsements regarding Belong’s products, returns (e.g., up to 6% p.a. including bonuses), tax benefits, or regulatory status under IFSCA. Users should independently verify all details, conduct due diligence, and consult qualified financial/tax advisors, as NuQuant accepts no liability for any decisions or losses arising from this information.